Dear Valued Shareholders,

This Management Discussion and Analysis (“MD&A”) is intended to provide the reader with operational and financial highlights of CCK Consolidated Holdings Berhad (“CCK” or “The Group”) for the financial year ended 31st December 2017.

The MD&A should be read together with the audited financial statements of the Group and Company.

- The retail segment will continue to focus on expanding its network of CCK stores in Sabah and Sarawak. With our consumers in mind, we are focused in providing a wider range of chicken cuts to suit the modern family’s lifestyle. We will focus on making our stores customer friendly by providing a comfortable environment for shopping and increasing our range of value-added products including custom cuts of chicken, beef and lamb.

- In order to support the retail segment’s expansion, the poultry segment will also be increasing its production of broilers and table eggs. Apart from increasing farm capacities, improving farm efficiencies and maintaining strict biosecurity measures would also continue to be emphasised and enhanced.

- In order to improve financial efficiencies, CCK’s loss-making operations in West Malaysia was closed in the last quarter of 2017. One new store was opened in 2017 in Debak, Sarawak. The retail network ended the financial year with a total of 55 stores across Sarawak and Sabah.

- In order to support the retail segment’s expansion, the poultry segment will also be increasing its production of broilers and table eggs. Apart from increasing farm capacities, improving farm efficiencies and maintaining strict biosecurity measures would also continue to be emphasised and enhanced.

- The poultry segment benefitted in 2017 from a stronger MYR/USD rate which lowered the cost of feed. In addition, the farm management tightened its processes to improve efficiency, thus increasing productivity.

Credit Risks

CCK practises a policy of dealing with creditworthy customers based on careful evaluation of each credit customer’s financial standing and credit history. This practice mitigates the risk of financial loss from possible default payments. The Group has also in place a credit monitoring process which regularly monitors the status and payments of our credit customers.

Foreign Currencies Fluctuation Risk

The Group imports frozen products for the network of retail stores where the purchases are denominated in US dollars. As such, the Group is exposed to currency fluctuation risk. Any adverse fluctuation in the MYR/USD rate may affect the profitability of the Group. In addition, fluctuations in the MYR/USD will likely affect the cost of feed for the poultry segment.

During the financial year ended 2017, the fluctuations in the MYR/USD were favourable compared to 2016.

Liquidity Risk

The Group maintains an adequate level of cash and cash equivalents and banking facilities to ensure sufficient liquidity to meet its liabilities as and when they fall due. The Group’s exposure to liquidity risk arises principally from trade payables, other payables and other bank borrowings (bankers’ acceptances and a revolving credit).

Competition Risk

CCK retail stores face increasing risks from existing and new competitors who offer similar products and compete on the basis of pricing. To mitigate this, we are continuously looking at means to improve our competitive edge. The Management not only focuses on pricing of products but also in evolving business models which improve the customers’ shopping experience.

Biosecurity And Disease Risk

Concerns regarding disease and biosecurity at our farms are constantly high on the agenda. The economic impact of a disease outbreak in any farm can be catastrophic on CCK’s bottom line. Constant monitoring is a compulsory standard operating procedure across all our operations even as we continuously innovate and update our biosecurity measures.

1. OVERVIEW

CCK Consolidated Holdings Berhad was incorporated as an investment holding company on 12th August 1996 and subsequently listed on Bursa Malaysia in 1997. CCK and its group of companies are principally involved in retailing and poultry farming. Our fully integrated supply chain consists of feed mill, breeder farms, hatchery, broiler farms, layer farm, abattoirs and retail stores. The businesses are carried out primarily in Sarawak, Sabah and Indonesia (Jakarta and Pontianak).

Since the opening of the first retail store in Sibu in 1970, our network of more than 50 retail stores now spans across Sarawak and Sabah. Fresh dressed chicken and chicken parts make up approximately 60% of our stores’ products. The remaining 40% of our stores’ products comprise frozen products, table eggs and fresh fruits and vegetables.

As Sarawak’s largest integrated poultry supplier our retail network is strongly supported by the poultry segment. CCK’s farm operations are also located in Sarawak and Sabah.

2. OBJECTIVES AND STRATEGIES

CCK continues to adhere to its main objective of creating a strong and profitable platform for the mutual benefit of all its shareholders and stakeholders based on the following 2-prong strategy –

Figure 1 Clean, dry and comfortable shopping environment

3. REVIEW OF FINANCIAL PERFORMANCE

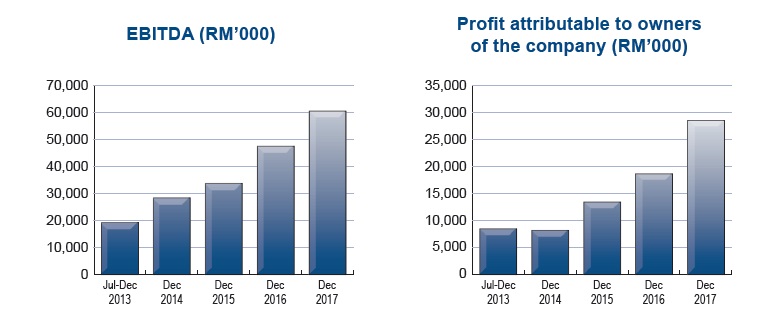

The Group’s revenue increased by 10.15% to RM615.789 million whilst profit before tax came in at RM38.636 million, an improvement of 52.26%.

Once again, the retail network spearheaded the Group’s revenue and net profit before tax with an improvement in revenue of 11.7% from RM424.7 million in 2016 to RM474.4 million in 2017. The Indonesian operations contributed 18% towards the Group revenue in 2017 as compared to 16% in 2016. Contributory factors leading to the better performance by the retail segment were better prices for chickens and table eggs.

CCK’s share of results in our associate, Gold Coin Sarawak Sdn Bhd rose from RM4.4 million in 2016 RM4.6 million in 2017.

During the financial year, total assets of the Group increased to RM380.660 million from RM364.153 million in 2016. The growth is mainly derived from increases in inventories and cash and bank balances.

4. REVIEW OF OPERATIONS

CCK believes that it should focus on strengthening and building on its core business areas. With the retail sector leading our operations and with strong support from the poultry sector, we are pleased to see much positive improvement in our results for 2017.

Figure 2 CCK Retail Network in 2017

5. ANTICIPATED OR KNOWN RISKS

6. DIVIDENDS

CCK has a dividend policy of paying up to 30% of the profit after taxation and minority interests and also considering the level of available funds, the amount of retained earnings, capital expenditure commitments and other investment planning requirements.

In line with our continued focus on shareholder returns, the Board is pleased to announce a first and final single-tier dividend of 3 sen per share for the financial year ended 31 December 2017.

7. OUTLOOK

Bank Negara Malaysia has raised its forecast for Malaysia’s economic growth in 2018 to 5.5% - 6.0% with a moderate overall inflation rate. Domestic demand is expected to drive the nation’s economic growth through continuous income and employment growth leading to sustainable household spending.

The above projections bode well for CCK. The strength of the CCK Group lies in its retail network supported by an integrated poultry supply chain. From feed mill, hatchery, breeder, broiler, layer, slaughtering house and finally, the retail outlet, our core chicken products are all sourced internally and we are able to ensure a consistent supply and best quality products for our retail stores.

Moving forward, CCK intends to expand its retail network in Sarawak and Sabah by opening a maximum of 5 stores in 2018. We will continue re-vamping out existing outlets by providing comfortable shopping environments and increasing the variety of fruits, vegetables, small packs of meat and chicken for the convenience of the our customers. In tandem with the proposed increase in the number of stores, broiler production will be enhanced with proposed new farms in Sarawak and Sabah.

The Indonesian operations will also continue its push by increasing its production of its core product ie sausages. In addition, a new nugget line will be added to boost our product variety.

In view of the above plans, the Board of Directors believe that the outlook for CCK remains positive for the coming financial year. The strength of the CCK brand particularly, in Sarawak and in Pontianak, Indonesia lies in the fact the we are able to provide fresh, good quality and diverse products in our stores. In Sabah, we are gradually gaining recognition amongst households and corporate customers as a trusted brand.

8. APPRECIATION

I would like to record my profound appreciation to my fellow directors on the Board, the management teams and the staff of the CCK Group of Companies for all their hard work and dedication. Their commitment and their tieless work have made CCK the success it is today. I would also like to acknowledge the support of our shareholders, business partners, suppliers and customers and thank you for your continued belief in CCK.